I started this blog with the premise to inform other fellow investors out there on how to stay ahead of market cycles. To me, investment strategy should be making sound estimation of market direction ahead of the all the news and crap you hear and read about. Because reacting to news is often too late.

Today's entry is very important to me because i try to understand why the market is reacting in certain ways and why the next big crash is constantly being delayed through manipulation by central banks around the world economic powers.

The graph above clearly shows S&P movement from March'09, as it moves up in steps every time a new Quantitative Easing is introduced. Naturally this is not healthy because of the external influence QE has on the market. And we are left with conflicting data, S&P should not be so high when we still have alot of companies with reduced PE ratios, earnings and growth decline.

If you are looking for value, Europe seems to be a better option than US and Japan. Europe is more than 15% cheaper then US in terms of its P/E ratio (EURO STOXX 50-15.57 , S&P 500 - 18.43) giving it room for higher profit.

Japanese market on the other hand, i personally will avoid because the monetary policy implemented will result in higher volatility (plus i dont really have the extra cash to gamble away).

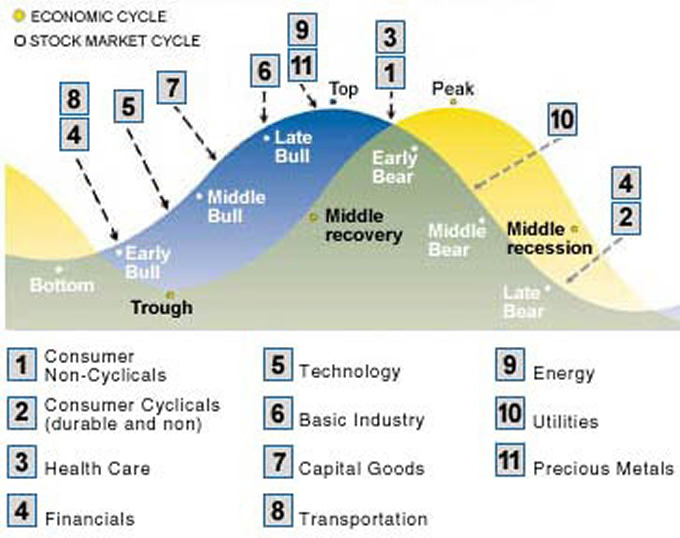

In these kind of scenarios with external influences, technical analysis becomes inaccurate and unreliable in my opinion. However one can still gear their investment strategy to pick the best sectors that perform well during late stages in a bull market. I need to pull up my favourite picture below which explains market cycles and recommendations:

I follow this graph very closely. We are in the late bull stages in the stock market cycle. For very good reason, there is no timeline on the x-axis because stock market cycle time can vary due to different influences. At this point of time i strongly recommend holding onto non-cyclicals defensive stocks such as utilities, consumer and healthcare.

I follow this graph very closely. We are in the late bull stages in the stock market cycle. For very good reason, there is no timeline on the x-axis because stock market cycle time can vary due to different influences. At this point of time i strongly recommend holding onto non-cyclicals defensive stocks such as utilities, consumer and healthcare.

Keep your eye on opportunities in cyclical stocks such as in the luxury goods, tech stocks and financials but dont buy them yet, wait till late bear market stages.

Dividend investing is always nice to have, keeping at least 30-40% of your portfolio based on regular dividend paying stocks is a strategy i adopt but keep a look out for dividend cuts, cancellations or script dividends.

To summarise, it seems the US market is already quite high, it would have to go to higher highs before the next market crash. This does not mean we should start worrying and panicking. The key thing would be to take profit where targets are reached, not to be greedy and keep at least 40% of your portfolio in cash by end of the late bull run. (Frankly no one knows when that might be, could be end of 2013 or could be after 1st Quarter of 2014)

Today's entry is very important to me because i try to understand why the market is reacting in certain ways and why the next big crash is constantly being delayed through manipulation by central banks around the world economic powers.

The graph above clearly shows S&P movement from March'09, as it moves up in steps every time a new Quantitative Easing is introduced. Naturally this is not healthy because of the external influence QE has on the market. And we are left with conflicting data, S&P should not be so high when we still have alot of companies with reduced PE ratios, earnings and growth decline.

If you are looking for value, Europe seems to be a better option than US and Japan. Europe is more than 15% cheaper then US in terms of its P/E ratio (EURO STOXX 50-15.57 , S&P 500 - 18.43) giving it room for higher profit.

Japanese market on the other hand, i personally will avoid because the monetary policy implemented will result in higher volatility (plus i dont really have the extra cash to gamble away).

In these kind of scenarios with external influences, technical analysis becomes inaccurate and unreliable in my opinion. However one can still gear their investment strategy to pick the best sectors that perform well during late stages in a bull market. I need to pull up my favourite picture below which explains market cycles and recommendations:

Keep your eye on opportunities in cyclical stocks such as in the luxury goods, tech stocks and financials but dont buy them yet, wait till late bear market stages.

Dividend investing is always nice to have, keeping at least 30-40% of your portfolio based on regular dividend paying stocks is a strategy i adopt but keep a look out for dividend cuts, cancellations or script dividends.

To summarise, it seems the US market is already quite high, it would have to go to higher highs before the next market crash. This does not mean we should start worrying and panicking. The key thing would be to take profit where targets are reached, not to be greedy and keep at least 40% of your portfolio in cash by end of the late bull run. (Frankly no one knows when that might be, could be end of 2013 or could be after 1st Quarter of 2014)